Issue #09

12 Jul 2026

Weekly Briefing |

GBTT.

Data. Not Vibes.

|

Great British

Think Tank

gbtt.info |

|

|

| Issue #09 · Sunday 12 July 2026 |

|

— Editor's Note

The most important news of the week is England beating Norway last night 2–1 to secure a place in the World Cup semi-finals.

In less important news, Britain has somehow ordered the full tasting menu: an energy shock from abroad, a domestic economy already wheezing, and a Bank of England preparing to raise rates into both. No substitutions.

Donald Trump declared the Iran ceasefire "over" on Wednesday. Within hours the US had hit ninety targets inside Iran — air defences, radar, missile sites, the Revolutionary Guard's fleet of small boats. Iran hit back at tankers, then at Qatar, Bahrain and Kuwait. Shipping through the Strait of Hormuz ground to a near-halt again. Oil jumped. Then it calmed down. Gilts did not. Ten-year yields touched 4.95% on Wednesday — the highest since 10 June. As I write, developing weekend events include the US striking 140 Iranian military targets overnight as Iran declares the Strait closed again, reinforcing the escalating troubles in the region.

Then Huw Pill went on BBC Walescast and said the quiet part out loud. Asked whether rates need to rise this year, the Bank's chief economist didn't hedge: "The short answer is yes." The economy, he said, has been running hotter than its supply side can sustain. Pill was one of only two MPC members who voted for a hike in June. Seven wanted to hold. The next meeting announcement is 30 July.

But there's a flaw in the plan. Higher rates don't manufacture oil. They don't reopen Hormuz. They don't persuade the Revolutionary Guard to stop attacking oil tankers. What they do is make mortgages dearer, credit scarcer, investment harder. Construction PMI: 38.4 in June. Below 50 means shrinking. This is a long way below it. Britain wants 1.5 million new homes. It is making the financing of building them steadily more expensive. Count Binface would call that insufficiently serious.

Gary Stevenson’s Channel 4 documentary, released last week, was meant to expose the super-rich. Instead, it exposed the dangers of giving a man who confuses QE with government spending an hour of television and no adult supervision. Perhaps we can now retire the wealth-tax debate before Channel 4 commissions a sequel.

Andy Burnham is expected in Downing Street on Monday 20 July as the new Prime Minister. Nigel Farage may soon be fighting Burnham, the bond market and Count Binface for airtime. Burnham promises to be "preventative, not crude" on welfare and pensions. Nice phrase. The Treasury’s answer will be shorter: no..

Mood music is cheap. Government is not.

|

|

— Image of the Week

ANN WIDDECOMBE, 1947–2026

Politics has lost one of its last conviction politicians. Ann Widdecombe pulled no punches, and you always knew where she stood. Westminster is poorer for her passing.

|

|

— The Big Story · OBR Fiscal Risks and Sustainability Report, 7 July 2026

Britain's Debt Bomb

Britain's fiscal arithmetic has finally caught up with its politics. The OBR says delay will only make the adjustment larger.

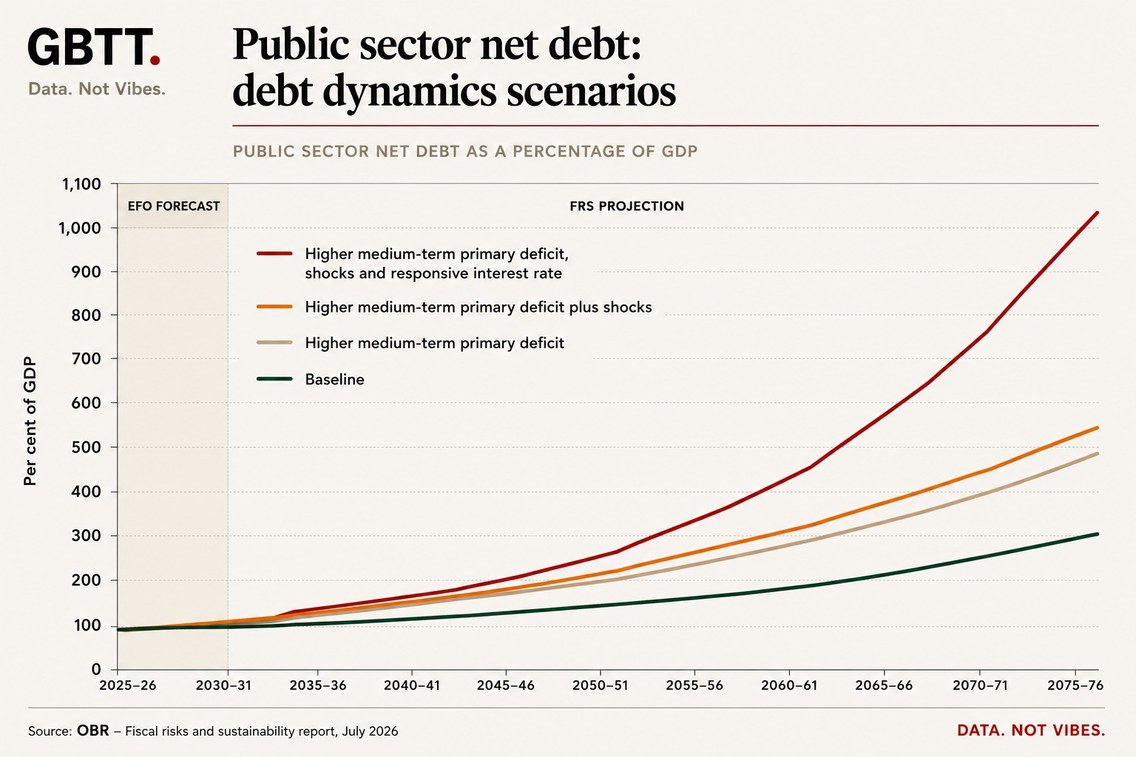

Public sector net debt: debt dynamics scenarios — OBR Fiscal Risks and Sustainability Report, July 2026.

|

Adjustment Needed

3.8% GDP

Permanent primary balance improvement from 2031–32 onwards to stabilise debt (baseline scenario) — not an annual add-on.

|

|

|

Scale, in Cash Terms

≈£115bn/yr

Around £4,000 per household, every year — roughly the entire education budget, or all onshore corporation tax receipts, in 2030–31 (OBR).

|

|

|

Delay Until 2050's

8% GDP

≈£8,000 per household in today's terms — close to the entire health budget. Waiting sends a larger bill to the next generation.

|

|

The OBR's warning is simple: if Britain carries on making the same spending promises without finding the money to pay for them, the national debt keeps rising for decades. In its central projection, debt climbs from around 95% of GDP at the start of the 2030s to roughly 300% by the mid-2070s. In a worse scenario, it rises above 500%. These are not forecasts in the normal sense. They are warning lights showing where current policy leads if governments, of all colours, refuse to change course.

The pressure comes from an ageing population, higher pension costs and ever-rising spending on health and social care. Tax revenues do not keep pace. The gap is filled by borrowing, which pushes up debt interest and leaves less money for everything else. In short, it's not sustainable on any measure.

The OBR says stabilising the debt would require a permanent improvement in the public finances equal to 3.8% of GDP from 2031–32, on top of what is already planned. In today's money, that is around £115bn a year — roughly £4,000 for every household in the country, every year. It would not necessarily arrive as a single bill. It could mean higher taxes, lower spending or more likely both. Delay until the 2050s and the adjustment rises to around 8% of GDP — more than £8,000 per household in today's terms. Waiting is not the painless option. It simply sends a larger bill to the next generation.

Westminster’s reflex is always the same: fiddle the fiscal rule, move the deadline, redefine the debt and conjure up a little more “headroom”. It is accounting theatre. Britain has built a state it cannot afford and lacks the honesty to say who will be made to pay for it.

Westminster can rewrite the rule as often as it likes.

It cannot repeal demography or compound interest.

|

|

— The Bank of England

A Tough Pill to Swallow

MPC rate-setter said in public what the Committee is still fighting about in private.

7–2

MPC vote to hold Bank Rate at 3.75% in June — Pill and Greene the two dissenters, both favouring a hike.

MPC members do not normally tell BBC Wales exactly what interest rates will do next. Huw Pill did. Asked directly whether rates would need to rise this year, the Bank's chief economist said: "The short answer is yes." That is about as close as a sitting rate-setter gets to pre-announcing a vote outside the Bank's own communications.

It also confirms how split the Committee already is. Pill and fellow external member Megan Greene were the two dissenters in June, both voting for a hike; the other seven preferred to hold. Two votes is not a majority. It is not nothing either.

Markets have already made up their mind about who is winning the argument. Money markets now price roughly a 75% chance of a hike by year-end, and ten-year gilt yields have pushed closer to 4.90%. Whatever the Committee's majority still says in public, the price action is backing the minority.

|

|

— Markets

Pill Says Rates Must Rise. Gilts Believe Him

Gilt yields are already doing the Bank's talking for it — and sterling is pricing the hike before the vote.

|

10yr Gilt

4.88%

|

30yr Gilt

5.60%

|

GBP/USD

$1.34

|

GBP/EUR

€1.174

|

FTSE 100

10,497

|

Sterling hit a one-year high against the euro and its best level against the dollar since 15 June, while the FTSE fell 1.7% on the week despite Friday gains in Vodafone (+12.7%) and easyJet (+14.1%) on deal news. Pill speaks again Monday; Bailey follows at Mansion House Tuesday — expect every word from both read as confirmation or pushback ahead of the 30 July MPC.

|

|

— Energy

Hormuz Traffic Collapses. Will The British Public Pay The Price Again?

Britain doesn't import inflation through oil. It imports it through gas — and that is how a war in the Gulf becomes a British electricity bill headache.

|

Hormuz Traffic

~5/day, it was ~130

|

Brent Crude (Fri)

$75.80

|

Cap, Now → Oct–Dec (Proj.)

£1,862 → £1,899

|

Shipping through the Strait has collapsed to a trickle: just five vessels crossed on Wednesday, according to maritime tracker Windward, down from roughly 130 a day before the war began in February. Brent itself has stayed comparatively calm — spiking over 5% intraday Wednesday to a two-week high near $78 before settling at $75.80 by Friday — but that calm is fragile, and it is already feeding into LNG prices just as households absorb July's 13% increase in the energy cap, an increase already baked in before this week's escalation. Cornwall Insight now projects the October–December cap around £1,899, about 2% above July's confirmed £1,862 — a forecast, not an Ofgem number; the regulator doesn't confirm the autumn cap until 26 August, and this week's escalation makes the direction more uncertain, not less.

Weekend update: Iran declares the Strait of Hormuz closed. Expect oil prices to spike on Monday.

|

|

— Further Reading

Two Pieces Worth Your Time

|

|

— GBTT Diary

CPAC Great Britain runs Thursday to Saturday at The InterContinental London, The O2 — GBTT represented by Senior Research Fellow Damian Pudner, speaking on rebooting Britain to restore growth and prosperity.

Pints and Policy, GBTT's new video podcast, launches in August on YouTube — keep an eye out for some excellent guests. Get on the list at gbtt.info to hear first.

|

|

— Next Week

Three Things to Watch Mon 13 – Fri 17 Jul 2026

| 1 |

Tuesday 14 July · Bank of England · 9pm

Andrew Bailey: Mansion House Speech

The Governor's first major remarks since Pill said rates will need to rise and gilt yields moved to price it in. Markets will parse every line ahead of the 30 July MPC.

|

| 2 |

Thursday 16 July · ONS · 7am

GDP, Index of Production & Construction Output: May 2026

The last output data before this week's Hormuz escalation feeds through — and the hard data behind this week's construction PMI signal.

|

| 3 |

Thursday 16 – Friday 17 July · Labour Party

Labour Leadership Nominations Close, Burnham Expected Confirmed

Burnham is expected to secure the leadership unopposed, clearing his route to Downing Street on 20 July.

|

|

|

GBTT.

Data. Not Vibes.

GBTT Weekly Briefing · Issue #09 · 12 July 2026

gbtt.info

Sources: ONS, Bank of England, S&P Global/CIPS, RICS, OBR, Cornwall Insight, Reuters, AP, Bloomberg.

Gilt yields, FTSE 100 and sterling: Friday 10 July close, Reuters. For information only. Not investment advice.

|

|