Issue #06

21 June 2026

Weekly Briefing |

GBTT.

Data. Not Vibes.

|

Great British

Think Tank

gbtt.info |

|

|

|

This Week

May borrowing £23.3bn — £5.6bn above OBR profile, debt interest a May record. MPC holds 3.75%, 7–2: Greene joins Pill as hawkish dissenters. Burnham wins Makerfield 55% on 59% turnout. Private-sector regular pay just 2.9%; whole-economy growth lifted partly by public-sector pay-award timing. Services inflation jumps 3.2% to 3.7%. Retail bounces +1.2%. 30-year gilt near 5.55% after a sharp Friday sell-off.

|

|

| Issue #06 · Sunday 21 June 2026 |

|

|

Three stories ran simultaneously this week: a borrowing miss, a hawkish MPC split, a by-election that has changed the political geometry.

Start with the money. May borrowing came in at £23.3bn — £5.6bn above the OBR’s profile. Two months in, accumulated borrowing of £46.3bn is £7.7bn above the £38.6bn forecast and £8.9bn higher than a year earlier. Debt interest reached £11.7bn in May alone — the highest for any May in nominal terms since records began. The index-linked gilt stock RPI uplift alone added £4.9bn to May’s interest bill. Net debt hit 95.1% of GDP.

Private-sector regular pay grew 2.9% in February to April, slightly below average CPIH inflation of 3.2% over the same period. The aggregate 3.4% figure was lifted by public-sector pay growth of 5.1%, which was partly affected by the timing of NHS pay awards. The unadjusted private-sector figure was below the Bank’s estimates of target-consistent wage growth, although an industry-mix adjustment raises the rate by roughly half a percentage point. This is little evidence of a renewed wage-price spiral. The MPC’s hawks disagreed: Greene joined Pill in voting for a 25bp rise, the first dual hawkish dissent since February 2024. Their case was reinforced by services inflation jumping from 3.2% to 3.7%, but rested more broadly on inflation expectations and the risk that the energy shock becomes embedded in domestic price-setting.

Then Burnham: 55% of the vote, 59% turnout, a majority of 9,231 against a 2024 Labour margin in the same seat of 5,399 — strong evidence of a substantial personal vote. On polling day, reports emerged that Richard Hughes, the former OBR chairman, was advising him on fiscal credibility. Gilts sold off sharply on Friday as borrowing data and political news arrived together. The arithmetic waiting for any new prime minister is brutal: income tax, VAT and employee NI are ruled out by the manifesto; the employer NI lever has been pulled; defence requires tens of billions more; welfare is one of the few remaining spending levers — and his instincts run the wrong direction on it.

Two guest opinion pieces will be published on gbtt.info later this week. Watch this space.

— Damian Pudner, Senior Research Fellow, GBTT

|

|

|

Watch

| |

Damian Pudner · GBTT

Powerless Central Bankers

Damian Pudner joins Gerald Ashley and George Cooper to discuss monetary policy, central-bank accountability and Britain’s deteriorating fiscal position.

|

|

|

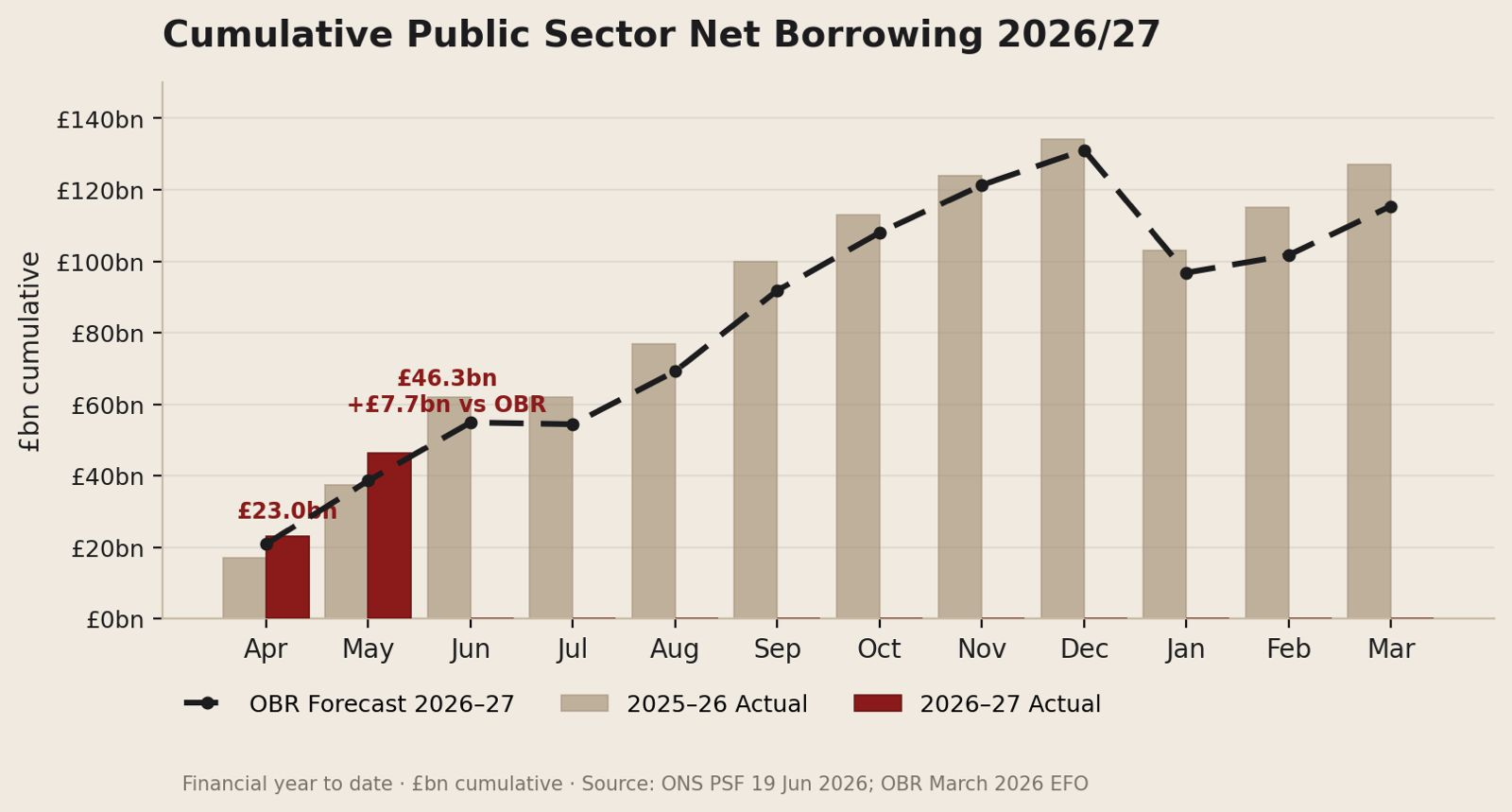

Chart of the Week

Two Months In. Already £7.7bn Above OBR Profile.

|

Cumulative Public Sector Net Borrowing 2026/27

Financial year to date · £bn cumulative · ONS PSF 19 Jun 2026; OBR Mar 2026 EFO

Grey bars: 2025–26 actual cumulative. Crimson bars: 2026–27 actual (April and May only). Dashed line: OBR March 2026 central forecast, cumulative. January dip reflects self-assessment income-tax receipts. Sources: ONS, OBR.

|

|

|

Public Sector Finances · ONS · Friday 19 June

May Borrowing £23.3bn. Debt Interest a May Record. Net Debt 95.1% of GDP.

|

May PSNB

£23.3bn

£5.6bn above OBR central profile (£17.7bn). April revised to £23.0bn, approx £2.1bn above profile.

|

|

|

Debt Interest (May)

£11.7bn

Highest May in nominal terms on record. Includes £4.9bn of RPI-linked capital uplift.

|

|

|

YTD Apr–May

£46.3bn

£7.7bn above OBR’s £38.6bn Apr–May profile. £8.9bn higher than the same period last year.

|

|

|

Net Debt / GDP

95.1%

Up from 94.2% in April. Highest on a comparable basis since the early 1960s.

|

|

Both months have missed. April borrowing was revised to £23.0bn, approximately £2.1bn above the OBR’s £20.9bn profile; May came in at £23.3bn against a profile of £17.7bn. The miss was broad-based: central-government expenditure exceeded profile, receipts were weaker than forecast and borrowing elsewhere in the public sector was also higher. Debt interest of £11.7bn was the standout — a May record in nominal terms, with £4.9bn reflecting the RPI-linked capital uplift following a 0.8% RPI increase between February and March. The OBR’s full-year borrowing forecast is £115.5bn, while central-government debt interest, net of the APF, is forecast at £109.4bn in 2026–27. That number remains acutely sensitive to persistent inflation and sustained increases in refinancing yields.

|

|

Inflation · ONS CPI · Wednesday 17 June

Headline Holds at 2.8%, but Services Jumps from 3.2% to 3.7%

|

CPI May 2026

2.8%

Unchanged from April. Second consecutive month at this level.

|

|

|

Services CPI

3.7%

Up from 3.2%. Travel and transport services, particularly air and sea fares, were the main upward influence.

|

|

|

Core CPI

2.6%

Up from 2.5% in April.

|

|

|

Goods CPI

2.0%

Down from 2.4%, with downward contributions from non-energy industrial goods and food-related categories.

|

|

The stable headline concealed a sharp divergence. Goods inflation fell from 2.4% to 2.0%, with weakness across non-energy industrial goods and food-related categories. Services did the opposite: 3.2% in April became 3.7% in May, driven by travel and transport, particularly air and sea fares, with Easter timing affecting the year-on-year comparison. Part of this move may reverse. But services disinflation has repeatedly proved uneven, core CPI is still edging up, and the May data gave the doves on the MPC very little to work with.

|

|

Labour Market · ONS June 2026 Release · Thursday 18 June

Private Sector Pay Just 2.9%. Slightly Negative in Real Terms. Vacancies at a Five-Year Low.

|

Unemployment (Feb–Apr)

4.9%

Up 0.3pp year on year. Down 0.3pp on the quarter. Employment rate 75.0%.

|

|

|

Private Sector Pay

2.9%

Regular earnings, Feb–Apr. Around 0.3% lower in real CPIH terms on a simple matched-period comparison.

|

|

|

Public Sector Pay

5.1%

Regular earnings, Feb–Apr. Partly affected by timing of NHS pay awards creating a base effect.

|

|

|

Whole Economy Regular

3.4%

Aggregate of public and private. Real CPIH: +0.1%. Including bonuses: 4.4%, real CPIH: +1.2%.

|

|

|

Vacancies (Mar–May)

707k

Lowest since February–April 2021. Down 19,000 on quarter. Consistent with continued gradual loosening.

|

|

|

Claimant Count (May)

1.71m

Up on both month and year. Provisional; subject to revision.

|

|

The public/private split is the number that matters most in this release. Private-sector regular pay grew 2.9%, slightly below average CPIH inflation of 3.2% over the same period. Whole-economy regular pay growth of 3.4% was lifted by public-sector growth of 5.1%, which was partly affected by the timing of NHS pay awards. On its face, private-sector pay was below the Bank’s estimates of target-consistent wage growth, although an industry-mix adjustment adds around half a percentage point. Vacancies fell to 707,000, the lowest since February to April 2021, adding to the evidence of gradual labour-market loosening. The Bank received these figures as exceptional pre-release data from 8:30am on Monday 15 June, ahead of the MPC meeting.

|

|

Monetary Policy · MPC Decision · Thursday 18 June

7–2 Hold at 3.75%. Greene Joins Pill. First Dual Hawkish Dissent Since February 2024.

|

BoE Base Rate

3.75%

Fourth consecutive hold since the December 2025 reduction.

|

|

|

MPC Vote

7–2

To hold. Greene joined Pill in voting for +25bp. Prior vote was 8–1 to hold.

|

|

Megan Greene joined Huw Pill in voting for an immediate 25bp rise — Pill had been the sole hawkish voice in April. The majority held because underlying disinflation appeared to remain intact, financial conditions had tightened, and weakness in activity and the labour market reduced the risk of second-round effects. The dissenters pointed to services inflation at 3.7% and the risk of second-round price pressure becoming embedded. The bar for a July cut has risen materially, although the decision remains contingent on energy prices, services inflation and evidence of second-round effects. Next decision: Thursday 30 July 2026.

|

|

Consumer · ONS Retail Sales & GfK · Friday 19 June

Retail Volumes +1.2% in May, Beating Consensus. April Revised Down to −1.0%.

|

Retail Volumes MoM (May)

+1.2%

Consensus: +0.5%. April revised to −1.0% from an initial estimate of −1.3%.

|

|

|

YoY Excl. Fuel

+4.6%

Annual volume growth, partly base-effect. Three-month trend: +0.4%.

|

|

|

Online Share

28.8%

Up from 28.1% in April. Non-store retail volumes +6.1% on the month.

|

|

|

GfK Consumer Confidence

−23

June. Unchanged for second consecutive month. Not a recovery signal.

|

|

Read May in context of April. The initial April release showed volumes fell 1.3%; the revised figure is −1.0%, making May’s bounce partly a recovery from a sharp decline. Non-store retail volumes rose 6.1% and warm weather lifted department stores; the headline beat the 0.5% consensus comfortably. Unchanged consumer confidence at −23, private-sector real wages slightly negative, and higher employment costs still weighing on the broader outlook: one month does not change the underlying demand picture.

|

|

Political Economy · Makerfield By-Election · Thursday 18 June

Burnham Wins 55% on Exceptional Turnout. Strong Evidence of a Personal Vote. Gilts Sell Off Friday.

|

Burnham Vote Share

55%

24,927 votes vs 15,696 for second-placed Reform. 2024 Labour majority here: 5,399.

|

|

|

Majority

9,231

More than 70% larger than the 2024 Labour margin. Strong evidence of a substantial personal vote.

|

|

|

Turnout

59%

Exceptionally high for a parliamentary by-election. Evidence of unusually strong voter mobilisation.

|

|

A 59% turnout and a majority 70% larger than Labour’s 2024 margin in the same seat is strong evidence of a substantial personal vote. On polling day, reports emerged that Richard Hughes — former OBR chairman — was among the economists advising Burnham on fiscal credibility. Gilts sold off sharply on Friday as borrowing data and political news arrived together. The fiscal arithmetic is unforgiving whoever holds the keys: income tax, VAT and employee NI are ruled out; the employer NI lever has been pulled; defence requires tens of billions more; welfare is one of the few remaining levers — and his instincts run the wrong direction on it.

|

|

Markets · Gilts & Sterling · Week to Friday 19 June

Gilts Rally Midweek Then Sell Off Sharply Friday. 30-Year Near 5.55%.

|

10Y Gilt

4.84%

Approx Friday close. Up approximately 9bps on the session, reversing earlier gains.

|

|

|

30Y Gilt

5.55%

Approx Friday close. Up approximately 9–10bps on Friday.

|

|

|

GBP/USD

1.3236

Approx 5pm BST Friday, Reuters. Recovered from session lows through the afternoon.

|

|

|

GBP/EUR

1.153

Approx 5pm BST Friday, Reuters. Broadly stable through the week.

|

|

|

FTSE 100

10,363

−0.35% Friday. Fell amid fiscal concerns and political uncertainty.

|

|

Gilts rallied through the middle of the week as ceasefire news in the Middle East eased oil prices. That reversed sharply on Friday when the borrowing data and Burnham’s result arrived together.

|

|

Data Calendar · 22–26 June 2026

Flash PMI on Tuesday Is the Signal Release of the Week.

22 Monday · June 2026

|

MED

09:30 BST

|

S&P Global UK Consumer Sentiment Index

S&P Global

|

23 Tuesday · June 2026

|

HIGH

09:30 BST

|

S&P Global / CIPS Flash PMI — Composite, Services, Manufacturing

| | |