Issue #05

14 Jun 2026

Weekly Briefing |

GBTT.

Data. Not Vibes.

|

Great British

Think Tank

gbtt.info |

|

|

| Context |

Ken Rogoff puts the probability of a UK debt crisis before 2030 at better than 50:50. Sir Charlie Bean calls an IMF bailout a “material risk”. The Treasury says both are wrong. Meanwhile: April GDP contracted, house prices are barely positive, and the MPC meets on Thursday with competing pressures on every side. |

|

— Editor’s Note

Ken Rogoff does not do hyperbole. The Harvard professor and former IMF chief economist said this week there is a “more than 50:50 chance” of a UK debt crisis before 2030. Sir Charlie Bean — a former Bank of England deputy governor — called an IMF bailout a “material risk”. The Treasury called it “completely untrue”. The Treasury is wrong to dismiss it so blandly, and Rogoff is right to say it out loud.

This is not about imminent catastrophe. It is about trajectory and shock-sensitivity. Public sector net debt sits at 94.2% of GDP, on a trajectory that, if maintained, would breach £3 trillion by September according to figures reported by the Telegraph. The OBR’s central forecast has net debt peaking near 96½% of GDP in 2028–29 before falling back towards 95% in 2030–31. That path assumes no further shocks. Rogoff’s point, which the Treasury cannot honestly refute, is that Britain has now absorbed three successive shocks — COVID, Ukraine, the Iran war — and each one has left the public finances in structurally worse shape. A fourth shock, on a 94% debt base, may not be manageable without external support.

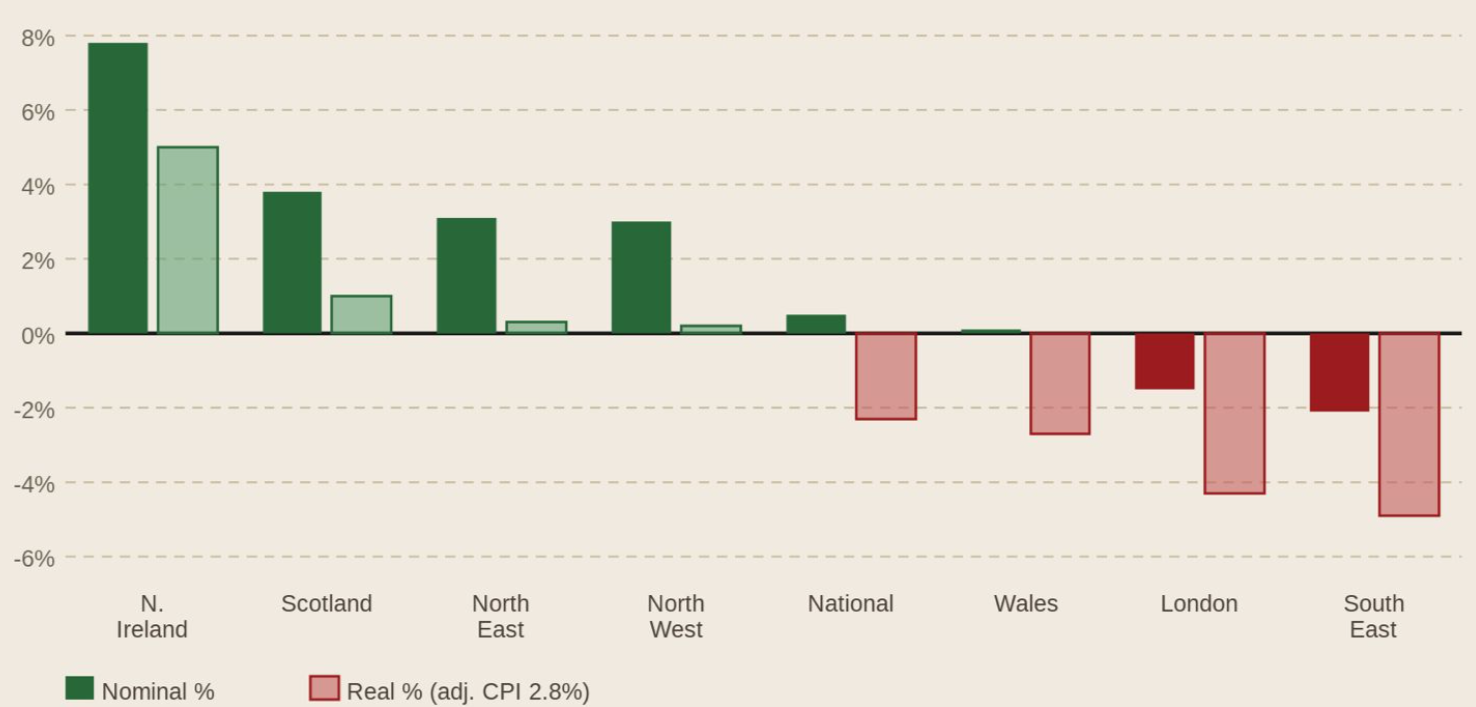

Against that backdrop, the rest of this week’s data is uncomfortable reading. April GDP fell 0.1% on the month — the first contraction since August 2025 — adding downside risk to the growth assumptions underlying the Spring Statement. Halifax put average house prices at £298,806 in May — +0.5% nationally but −2.1% in the South East and −1.5% in London. The regional fracture is this week’s chart. The welfare bill grows. Debt interest accrues. The MPC meets on Thursday against a backdrop in which holding at 3.75% is simultaneously prudent and insufficient to resolve the underlying problems.

Yet another potential US-Iran peace agreement — unsigned at the time of writing — drove Friday’s equity rally and oil sell-off. If signed, lower energy costs would provide genuine near-term relief. Britain’s structural energy cost problem does not disappear with a resolution. But the week’s dominant story was not whether the deal is actually signed. It was two serious economists putting a number on the probability of a crisis that the political class has spent years pretending cannot happen.

|

|

This Week on GBTT

| |

Guest Opinion · Ben Ramanauskas

Picking Losers: The Return of Britain’s Industrial Strategy Delusion

Ministers want the state taking equity stakes in Britain’s fastest-growing tech firms. Ben Ramanauskas on why picking winners has never worked, and why it won’t this time. Read →

|

|

|

Watch

| ► |

The Liz Truss Show · Damian Pudner

Britain’s Broken Model — and What It’s Going to Take to Fix It

I recently sat down with Liz Truss to discuss the case for radical supply-side reform, BoE mandate accountability, and why you cannot tax and spend your way to growth. Watch on YouTube →

|

|

|

Chart of the Week

A Market Fracturing

Halifax House Price Index · May 2026 · Annual % Change by Region

Annual % change — nominal (solid) and real (lighter, adjusted for CPI 2.8%) — by region, May 2026

Source: Halifax House Price Index, May 2026 (released 5 June 2026) · Regional figures are three-month rolling annual comparisons, not directly equivalent to Halifax’s seasonally adjusted monthly national series · Real = nominal − CPI (April 2026: 2.8%) · Simple subtraction

|

|

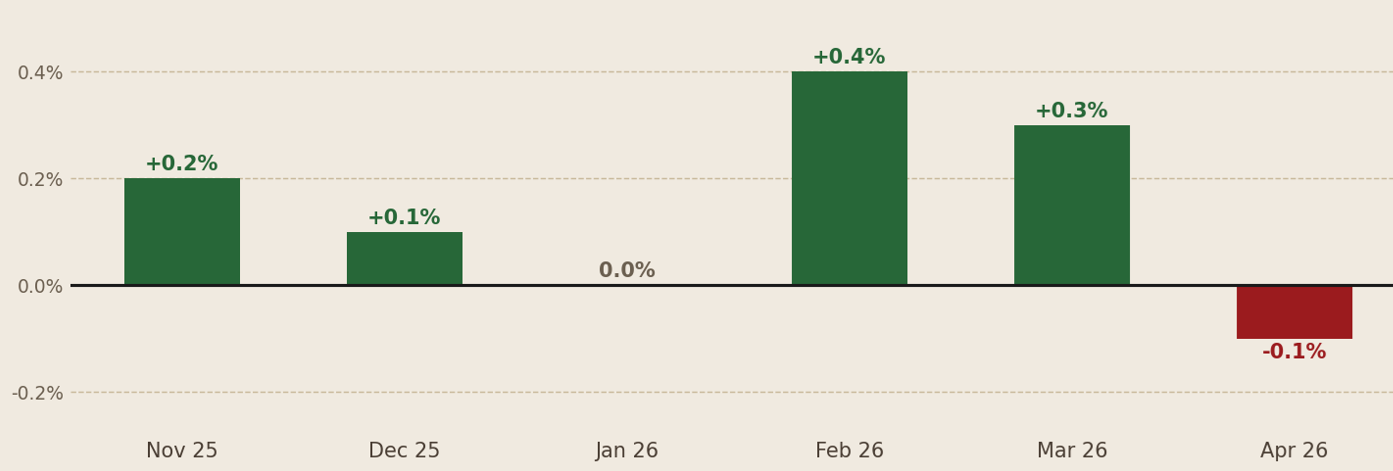

Economic Output

April Stumbles: GDP Contracts for First Time Since August

ONS GDP Monthly Estimate · April 2026 · Released 12 June 2026

Monthly change −0.1% April 2026. First monthly fall since August 2025. |

Year on year +1.2% April 2026 vs April 2025. Same pace as March. |

3-month growth +0.7% Feb–Apr vs Nov–Jan 2026. Fifth consecutive positive rolling period. |

Services −0.2% Main drag. Admin & support −2.2%. Arts & recreation −4.3%. |

Monthly GDP growth (%) — November 2025 to April 2026

Source: ONS GDP Monthly Estimate, UK: April 2026 · Released 12 June 2026 · Seasonally adjusted chained volume measure

GDP fell 0.1% in April 2026, the first monthly contraction since August 2025 and the result investors feared after May’s final services PMI slipped to 49.3. The principal drag was services, where administrative and support services fell 2.2% and arts, entertainment and recreation fell 4.3% — sectors that are acutely sensitive to consumer confidence and business spending. Information and communication rose 1.1%, providing partial offset. Construction added 0.1%. Production was flat.

The three-month picture (February to April versus November to January) remains positive at +0.7%, the fifth consecutive positive rolling period. That cushion matters: the ONS and Bank of England will lean on it to argue the April contraction is noise rather than signal. That argument has merit — February grew 0.4% and March 0.3%, so April represents deceleration after a strong run rather than a collapse. But the forward indicators — services PMI at 49.3, DMP expectations for employment growth weakened to −0.3% in the three months to May, hiring intentions weakening — suggest April is unlikely to be the low point of the softening.

|

|

Gilt Markets & Sterling

Long End Elevated, Ten-Year Falls Back

Friday 12 June 2026 · 5pm Close

10yr Gilt Yield 4.83% Friday 12 June close. Fell sharply on Iran peace-deal hopes and lower oil prices. |

30yr Gilt Yield 5.54% Long end remains elevated. Duration risk and fiscal premium still embedded. |

FTSE 100 10,471 +1.6% on day. Iran deal optimism lifted all major indices. |

GBP / USD 1.3412 Sterling steady. GDP softness contained by Iran deal risk-on. |

GBP / EUR 1.1584 Euro broadly firm as risk appetite improved across Europe. |

BoE Base Rate 3.75% Held since December 2025. Next decision: Thursday 18 June. |

The FTSE 100’s 1.6% Friday rally — closing at 10,471 — was driven almost entirely by the Iran peace-deal narrative rather than domestic fundamentals. The GDP contraction was the first hard macro data of the session; the market processed it quickly and moved on to geopolitics.

|

|

Global Context

Rogoff, Bean, and the IMF Question

Rogoff / Bean Warnings · Published 6–9 June 2026 · World Bank GEP June 2026

Global Growth 2026 2.5% World Bank GEP June 2026. Down from 2.9% in 2025. Weakest since COVID onset. |

Rogoff: Crisis Probability >50% “More than 50:50 chance of a UK debt crisis before 2030.” — Prof. Ken Rogoff, Harvard / former IMF chief economist. |

UK Debt, Nominal £3tn On the trajectory reported by the Telegraph, nominal net debt could breach £3 trillion by September 2026. |

Bean Assessment Material Sir Charlie Bean (former BoE deputy governor): IMF bailout now a “material risk”. |

Rogoff’s warning is precise: successive shocks — COVID, Ukraine, the Iran conflict — have left Britain exposed to a greater than 50% probability of a fiscal crisis before 2030, requiring massive tax rises or spending cuts. If the Bank lost control of inflation, he said, the UK would “probably” need IMF support. Sir Charlie Bean — former Bank of England deputy governor and OBR member, not given to catastrophism — called it a “material risk”.

The Treasury’s response: “completely untrue.” That is not an argument. The IMF’s Staff Concluding Statement of the 2026 Article IV Mission — published 18 May — warned that the consolidation path faced implementation risks on both the expenditure and revenue sides, including uncertain tax bases and ambitious savings assumptions. The subsequently released April borrowing and GDP figures add to those risks; they were not considered in the IMF’s statement. The World Bank cut the global growth forecast to 2.5% for 2026 — weakest since 2020 — citing Middle East energy disruption and trade friction.

The 1976 parallel is imprecise but not irrelevant. In 1976, the UK went to the IMF with debt at around 55% of GDP. It is now at 94.2% and rising. Rogoff’s claim is not that crisis is inevitable — it is that the probability has risen enough to warrant honest discussion. The Treasury’s instinct to shut that down is understandable. It is not credible.

|

|

Housing & Property

RICS: Stabilising at Low Levels

RICS Residential Market Survey · May 2026 · Released 11 June 2026

Price Balance −35% Net balance of surveyors reporting price rises rather than falls. Unchanged from April. |

New Buyer Enquiries −34% Net balance. Demand deeply negative — no meaningful recovery in buyer interest. |

New Instructions −8% New instructions still falling — supply is not building despite price pressure. |

Sales Agreed −37% Extremely weak. Agreed sales running at near-recessionary levels of activity. |

12-Month Price Outlook +6% Marginally net positive for the year ahead — conditional on rate cuts materialising in our opinion. |

Avg New Mortgage Rate 4.08% April 2026 (BoE data). Above pre-2022 norm. Affordability constraint. |

A minus 35% price balance is not a housing market in recovery; it is one in orderly retreat. Mortgage rates have risen again — the average new mortgage rate reached 4.08% in April — and the backdrop of Middle East uncertainty continues to suppress buyer confidence in higher-value markets.

|

|

Last Week’s Data

Work Capability: The UC Health Caseload Surges

DWP · UC Work Capability Assessment Statistics · Published 11 June 2026 · Data to March 2026

UC Health Caseload 3.5m People on UC with a health condition or disability, March 2026. Up 34% (890,000) in the year. |

Share of All UC Claimants 42% Up 8 percentage points in a single year. North East: 47%. London: 35%. |

LCWRA Caseload 78% 2.8 million assessed as LCWRA — not required to undertake any work-related activity. |

Annual Increase +34% Net caseload increase of 890,000 in the year. 72% of the rise driven by ESA transitions onto UC. |

Mental Condition Recorded 71%+ At least 71% of non-ESA-transition WCA decisions included a recorded mental and behavioural disorder. DWP cautions that this may not be the claimant’s primary condition and that medical-condition recording is incomplete. |

Total WCA Decisions 4.6m Since April 2019. 12% found capable for work; 72% awarded LCWRA (most restricted). |

|

|

From our friends at CPAC

CPAC comes to Britain

The world’s most influential conservative gathering — London, July 2026

|

|

The inaugural CPAC Great Britain takes place 16–18 July 2026 at The InterContinental London, The O2, Greenwich. For the first time, the world’s most influential conservative gathering is crossing the Atlantic, bringing together leading voices from the UK, the US and across Europe for three days of speeches, debates and ideas.

On the agenda: free speech, economic freedom, pushing back against the establishment, and what it’s going to take to restore Britain.

| |

Confirmed speakers

Nigel Farage · Sir Jacob Rees-Mogg · Ambassador Ric Grenell · Mateusz Morawiecki

|

On the evening of Friday 17 July, 500 guests will sit down for the Sir Winston Churchill Gala Dinner — a prestigious black-tie event in honour of Britain’s greatest wartime leader. Tickets include Gold and Silver VIP options with premium access across all three days.

|

|

|

|

Data Calendar

What’s Coming: 15–19 June 2026

| Wednesday 17 June 2026 |

|

HIGH

7:00am

|

Consumer Price Inflation, UK: May 2026

ONS · CPI / CPIH / Core / Services

April was 2.8%.

|

| Thursday 18 June 2026 |

|

HIGH

7:00am

|

Labour Market Overview, UK: June 2026

ONS · Unemployment, pay growth, payrolled employees, vacancies

|

|

HIGH

Noon

|

Bank of England MPC Rate Decision

Bank of England · Monetary Policy Committee

Hold at 3.75% expected

|

| Friday 19 June 2026 |

|

HIGH

7:00am

|

Retail Sales, Great Britain: May 2026

ONS · Volumes, ex-fuel, year-on-year

April fell 1.3% month-on-month.

|

|