Issue #08

5 Jul 2026

Weekly Briefing |

GBTT.

Data. Not Vibes.

|

Great British

Think Tank

gbtt.info |

|

|

| Context |

Energy bills rose 13% from Wednesday. Mortgage approvals hit a 29-month low. Money supply (M4ex) growth ticked up to 4.8%. Gilts sold off following Bailey's Sintra remarks. Hormuz transit remains constrained. Burnham's leadership nominations open Thursday. |

|

| Issue #08 · Sunday 5 July 2026 |

|

Burnham spent Friday taking questions on Reddit. That is apparently how you audition for Number 10 now.

More than 2,000 questions came in; he picked the ones he fancied. Two lines mattered. No early general election. And the triple lock stays: “it is important that the commitment in the manifesto stands.” Fine words, delivered two days after Starmer handed him a Defence Investment Plan with a £4.7bn hole in it. The Treasury’s own line is that the gap gets sorted in “the next budget” — which will not be Starmer’s. Burnham had asked for the release to be delayed so he could deal with it himself. He found out the actual number the same day the rest of us did. That is not a parting gift. It is a parting shot.

Mortgage approvals fell 15% in May, while broad money growth rose from 4.6% to 4.8%. Those two figures point in different directions. Housing is slowing sharply, while the amount of money in the wider economy is growing faster. The Bank’s inflation-targeting framework pays remarkably little attention to that distinction.

The business surveys were weak. Services slipped into contraction, with the PMI falling to 48.8, while the wider composite index dropped to 49.3 — its weakest reading since April 2025. In plain English: the private economy is losing momentum.

Andrew Bailey used his Sintra remarks to push back against early rate cuts, even as he acknowledged the economy is softening. Gilts sold off. The ten-year yield rose to 4.80%; the thirty-year to 5.48%.

So the next leader inherits weaker growth, expensive borrowing, a still-disrupted Strait of Hormuz despite falling oil prices, and a live US threat of 100% tariffs over Britain’s £700m-a-year digital services tax.

GBTT passed 10,500 followers on X — we said 10,000 by year end and got there six months early. Thank you! We’ve also added a money tracker to the homepage for the monetarists, the money supply being the variable that actually moves inflation and the economy. Data should be timely, not reproduced a month after release.

|

|

|

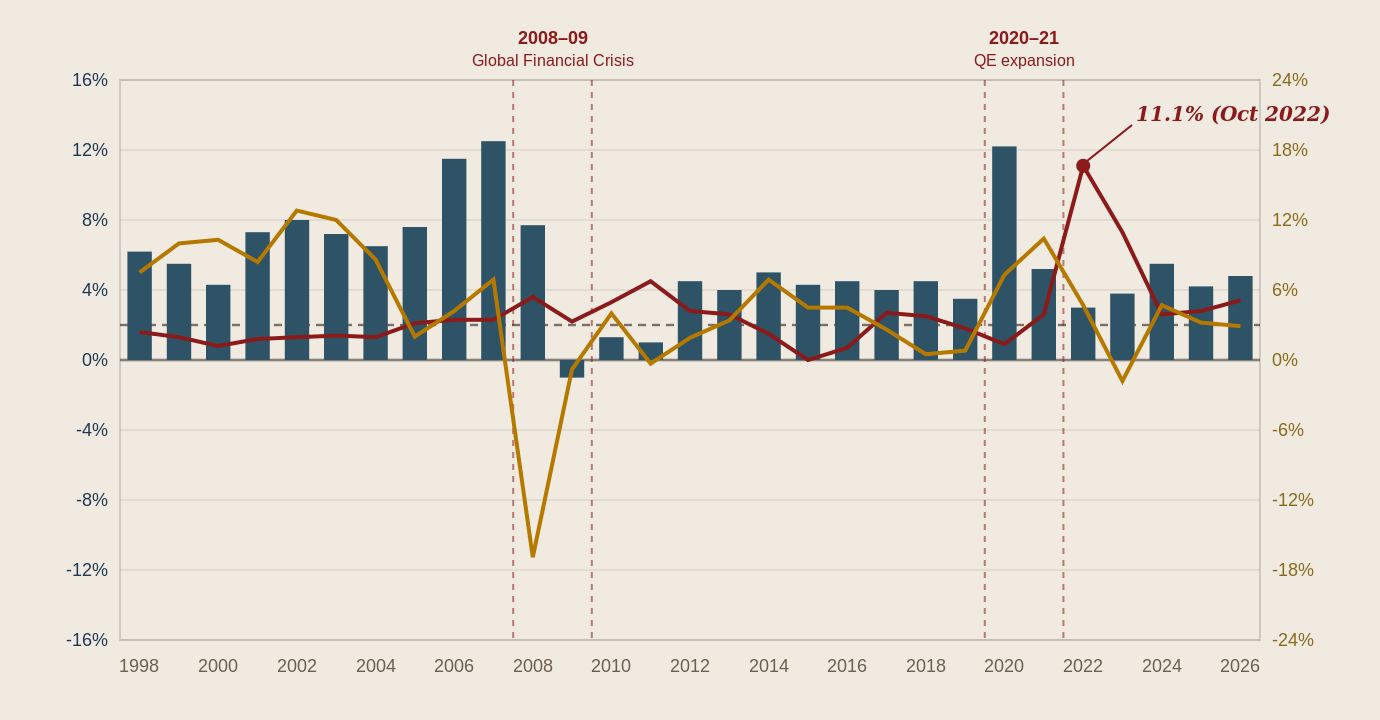

— Chart of the Week

Money Supply, Inflation & UK House Prices

|

Annual growth rates: M4ex, CPI inflation and Nationwide House Price Index · 1998–2026

M4ex growth (left axis)

CPI (annual inflation, left axis)

Nationwide house prices (right axis)

2% BoE target

| KEY TAKEAWAY: Rapid money growth during 2020–21 was followed by the inflation surge of 2021–22. House prices responded earlier and more quickly, before weakening as monetary growth slowed and interest rates rose. |

Annual growth rates shown at calendar year-end unless stated. M4ex and CPI figures for 2026 are the latest available (May 2026); Nationwide HPI is to June 2026. This reproduces GBTT’s long-run reference chart; readers wanting the underlying series should go to the primary sources below. Sources: Bank of England (M4ex), ONS (CPI), Nationwide Building Society (House Price Index).

Full money supply release →

|

|

|

|

— Money & Credit · BoE, May 2026 · Monday 29 June

Mortgages Freeze Up While Broad Money Warms Up

|

Mortgage Approvals

56,200

Down 15% from 66,000 in April. Lowest since December 2023.

|

|

Net Mortgage Borrowing

£2.9bn

Down from £4.4bn in April. Weakest in a year.

|

|

Remortgage Approvals

33,300

Down from 51,200 in April. A sharp retrenchment in refinancing activity.

|

Mortgage approvals fell 15% in May. Bank Rate is unchanged at 3.75%, but housing credit is tightening sharply. The twist is that broad money is no longer contracting: M4ex rose £11.0bn on the month and annual growth edged up to 4.8%. The Bank has a housing slowdown, not a simple monetary squeeze.

|

|

— Energy

The Energy Shock Has Reached Household Bills

|

Price Cap (from 1 Jul)

+13%

Typical annual bill: £1,663 under Ofgem’s revised consumption measure, up 13%.

|

|

Gas Bills

+24%

The main driver of the increase.

|

|

Electricity Bills

+5%

A smaller but still material rise.

|

Higher wholesale gas prices linked to the Middle East conflict are now feeding through to household bills. The Bank of England cannot produce more gas or reopen a shipping route by changing Bank Rate. But the rise comes just as mortgage borrowing is slowing sharply and household energy debt has hit a record £4.8bn. Another squeeze on household finances.

|

|

— Gilt Markets & Sterling

Bailey Says Rate Cuts Are Still Off the Table. Gilts Give Back the Rally

| Move |

10yr gilt rose from approximately 4.74% (Friday 26 June close) to approximately 4.80% (Friday 3 July close) following Bailey’s Sintra remarks. 30yr rose from approximately 5.39% to approximately 5.48%. BoE base rate: 3.75%. Next MPC decision: Thursday 30 July 2026. |

|

10yr Gilt (Fri close)

4.80%

Up ~6bps on the week, reversing part of the prior week’s rally.

|

|

30yr Gilt (Fri close)

5.48%

Up from ~5.39% last week. Long-term government borrowing costs remain exceptionally high.

|

|

BoE Base Rate

3.75%

Held since December 2025. Last vote in June: 7–2 to hold; Greene and Pill wanted a hike to 4%.

|

| |

|

GBP / USD

1.328

Up from 1.3204 last Friday. More dollar softness than sterling strength.

|

|

GBP / EUR

1.167

Up from 1.1585 last week. Range 1.156–1.170 through the week.

|

|

FTSE 100

10,679

Reuters/LSE Friday close, up from 10,437 last week. Thursday alone rose 1.76%.

|

Bailey was blunt: “There was an expectation that we would cut rates this year. That's not unreasonable in the context of a softening economy. That was off the table in March, and it's off the table at the moment.”

|

|

— Political Economy

Nominations Open Thursday. So Does the Defence Black Hole

|

Leadership Nominations

9 Jul

Open Thursday, close 16 July. Burnham has 200+ MPs’ backing, no declared challenger.

|

|

Defence Funding Gap

£4.7bn

Unfunded in the £298bn Defence Investment Plan, per the Treasury. To be resolved “in the next budget.”

|

|

New Leader By

29 Aug

Could conclude 17 July if Burnham stands unopposed once nominations close.

|

Starmer stays on as caretaker for now. The £298bn Defence Investment Plan he published Tuesday — budget up £15bn — comes with a £4.7bn hole the Treasury admits is unfunded. Burnham had asked for the plan to be held back so he could handle it himself; instead he learned the real number on release day, same as everyone else. On Friday’s Reddit Q&A he promised the plan would be “fully funded”, ruled out an early general election and reaffirmed the triple lock. He did not say how the £4.7bn — or the welfare bill, the largest obvious place left to look once tax and defence commitments are taken as given — actually gets paid for.

|

|

— Westminster · gbtt.info Chart of the Day, 3 July 2026

The Moonlighting Class: Outside Earnings Have Gone From Habit to Norm

|

Conservative

49.1%

Was 36.6% in 2014.

|

|

Labour

45.4%

Was 16.7% in 2014.

|

| |

|

Lib Dem

59.7%

Was 26.3% in 2014.

|

|

Reform

62.5%

n=8 MPs. No comparable 2014 figure — the party did not exist in its current form.

|

Share of each party’s MPs with declared outside earnings, 2014 versus 2026. Outside earnings are no longer a Westminster fringe activity, despite Labour’s 2024 pledge to curb paid advisory and consultancy roles — the party’s own MPs have nearly tripled their rate of declared outside income since then. Read the full chart →

|

|

— Guest Opinion

This Week on gbtt.info

|

Housing · 3 July 2026 · 7 min read

1.34m households sit on the social housing waiting list, but the verified floor of acute need is just 130,000–338,000. Read →

|

|

Tax · 30 June 2026 · 6 min read

Norway’s exit tax didn’t stop wealth leaving — it just exported it: 261 left in 2022, 254 in 2023. Read →

|

|

Europe · 29 June 2026 · 8 min read

Britain opted out of direct equity instruments when it rejoined Horizon Europe, so buying into the EU’s €5bn Scale Up Fund would likely need a treaty change. Read →

|

|

Comment · Reprint from CapX · 2 July 2026 · 6 min read

A 60% marginal rate hidden between £100,000 and £125,140 — the case for one rate, one generous allowance, no cliff edges. Read →

|

|

|

— From Our Friends at CPAC

|

From Our Friends at CPAC

CPAC Comes to Britain

The world’s most influential conservative gathering — London, July 2026

|

|

The inaugural CPAC Great Britain takes place 16–18 July 2026 at The InterContinental London, The O2, Greenwich. For the first time, the world’s most influential conservative gathering is crossing the Atlantic, bringing together leading voices from the UK, the US and across Europe for three days of speeches, debates and ideas.

On the agenda: free speech, economic freedom, the threat of Islamism, pushing back against the establishment, and what it’s going to take to restore Britain.

|

Confirmed Speakers

Nigel Farage · Sir Jacob Rees-Mogg · Ambassador Ric Grenell · Mateusz Morawiecki

|

On the evening of Friday 17 July, 500 guests will sit down for the Sir Winston Churchill Gala Dinner — a prestigious black-tie event in honour of Britain’s greatest wartime leader. Tickets include Gold and Silver VIP options with premium access across all three days.

|

| Gala dinner enquiries: [email protected] · Tables of 10 from £6,000 |

|

|

|

|

— Big News

GBTT Is Going to Video. Pints and Policy Launches Soon

| Launch |

Over 10,500 of you now follow GBTT on X. Soon you’ll be able to watch us too. 'Pints and Policy' is our new video podcast: three people, a drink, and a proper conversation about the economics, politics, and the issues shaping Britain. |

No autocue. No formal studio panel. No seven-second answers. We want to explain the numbers, argue about what they mean and make economics accessible to people who do not spend their day reading ONS releases or watching bond markets.

|

Format

Unscripted

Long-form conversation, not clips built for algorithms.

|

|

Platform

YouTube

Free to watch. Search GBTT when it lands.

|

|

Launch Window

Coming Soon

In production now. Subscribers hear first.

|

Get on the list at gbtt.info and you’ll be the first to know when episode one drops.

|

|

— Data Calendar

Next Week Mon 6 Jul — Fri 10 Jul 2026

| Tuesday 7 JULY 2026 |

| MED |

BRC–KPMG Retail Sales Monitor, June 2026

BRC

|

| Thursday 9 JULY 2026 |

| MED |

RICS UK Residential Market Survey, June 2026

RICS

|

| MED |

ONS Real-Time Indicators

ONS

|

A thin week for tier-one data. BRC-KPMG on Tuesday and RICS and the ONS real-time indicators on Thursday are the releases that clear the HIGH/MED bar. Thursday also sees Labour’s nominations open; a Commons defence debate lands Wednesday 8 July. Neither is a data release, but both will move the politics priced into gilts.

|

|

GBTT.

Data. Not Vibes.

GBTT Weekly Briefing · Issue #08 · 5 July 2026

Senior Research Fellow: Damian Pudner

Great British Think Tank · gbtt.info

Sources: ONS, Bank of England, OBR, RICS, S&P Global/CIPS, Reuters, Bloomberg.

Market prices are approximate 5pm BST Friday closes. For information only. Not investment advice.

|

|